Dear friends,

we have just attended to the World Tomato Conference held in Greece.

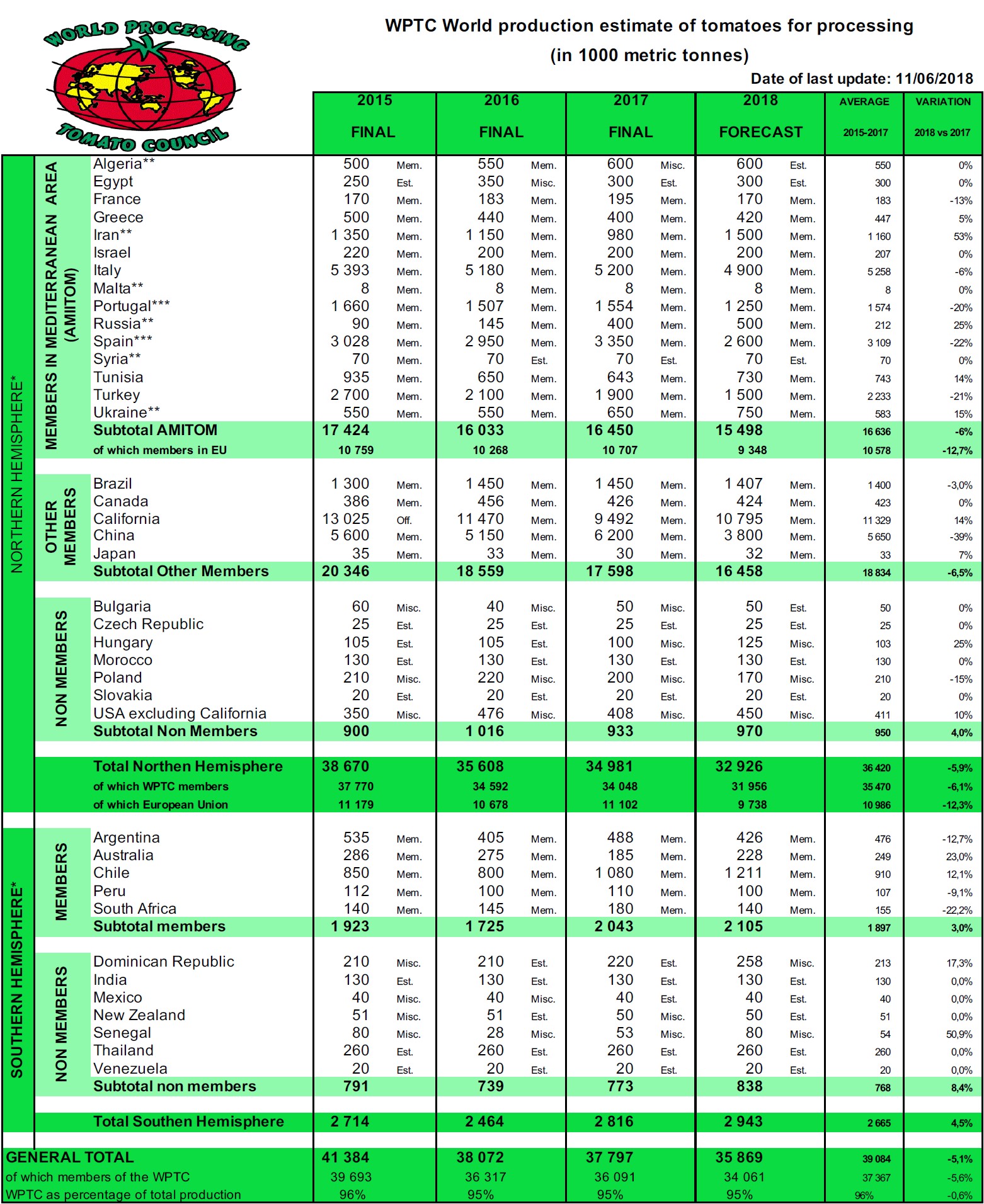

The official reports are confirming the following production forecast:

You can notice a substantial production reduction in comparison with those of last years.

Main surprising and important information is coming from China. As you can see the document is declaring a forecast of 3.8 millions tons fresh tomatoes equivalent (our personal forecast is max 3.6) that is 2.4 millions below last year.

It is very important to note that this is not connected to an adverse weather condition but to a real lower planning due:

1) the second largest producer Chalkis (just for financial reasons) will not produce this year that is they are going to stop about 13 factories!

2) The central government has imposed a very strict control of the environment rules connected to the water treatment and smoke emissions. Many small factories were unable to comply with above rules because the investments required were not sustainable in view of their small production

The conference was finally disclosing a very important news regarding the global consumption which is in fact lower than expected.

For many years the model for the tomato industry was connected to a constant consumption increase at the rate of about 2% per year and this was compensating the natural push to increase the production also following the logic “more you produce lower is your cost”.

Already in our last report dated July 2017 we were suggesting a steady global consumption at about 38 millions tons but now we believe we have to adjust this number to a lower level.

During the conference a consumption at about 37 millions was suggested.

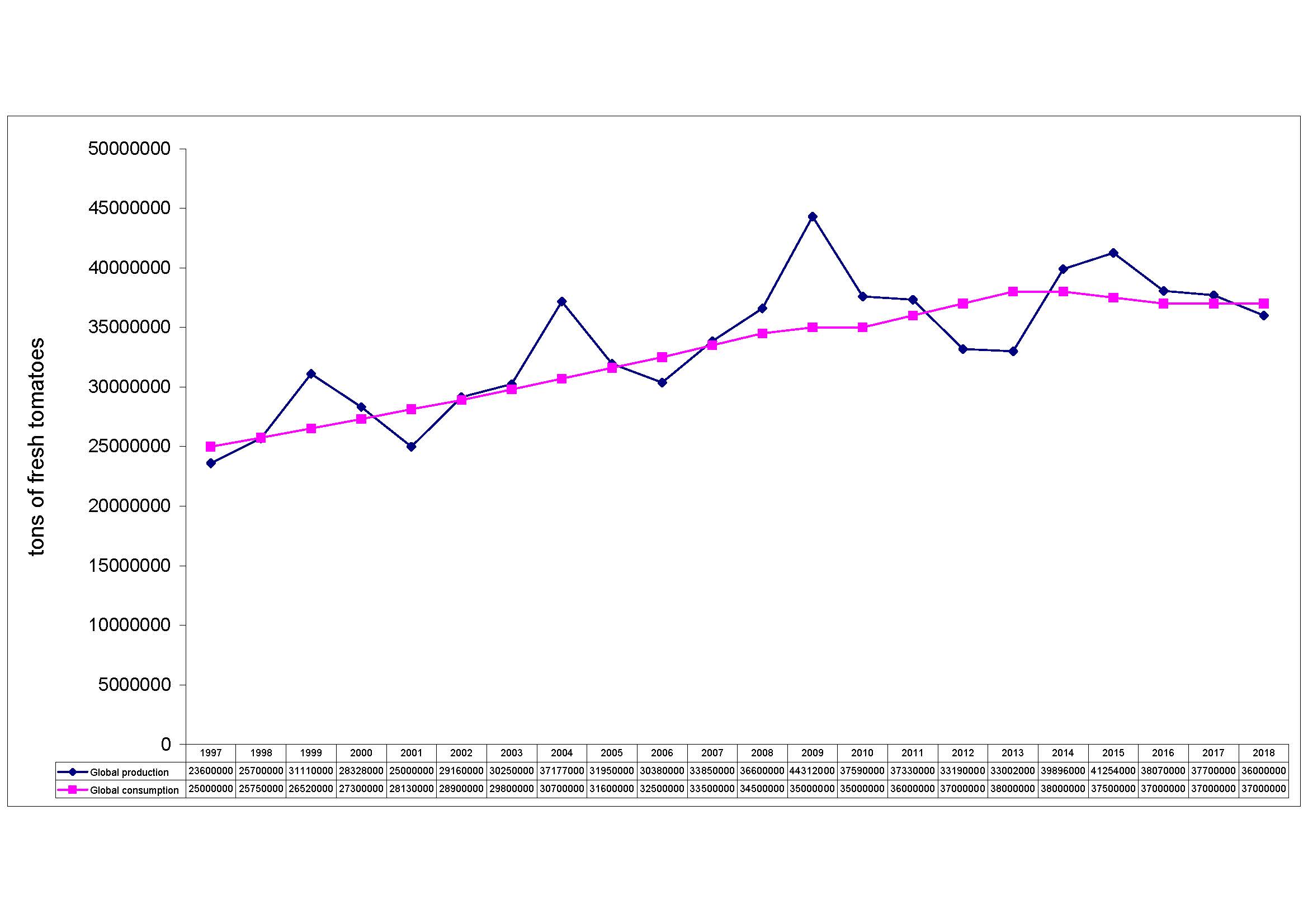

Consequently our graph crossing production and consumption should be modified as follows:

Of course as far as concerns the consumption the above numbers are probably not exactly matching the reality but for sure giving you a right feeling of the today problems.

Following our experience and independently from the statistics please follow our logic: just before the crop 2014 the world market was more or less in balance, at that time prices were very high and it was very difficult to find product available for those customers looking for prompt shipment. The market was more or less in balance.

So our suggestion for this simple exercise is to take that reference as a starting point of our analysis:

1) during the crop 2014 – 2017 we have produced a global quantity equivalent to about 156,920,000 tons

2) during the same period according to the above estimate, the consumption was equivalent to about 149,500,000 tons

3) the difference between the above numbers is bringing a total carryover on top of what it was available at the start of crop 2014 of about 7,420,000 tons fresh tomatoes equivalent.

In our opinion that number is possibly very close to the reality. We can say for sure that the combined extra carryover in China and California is at least equivalent to 4 millions tons and the rest can be easily found among all other markets.

Following the above logic and reported statistics we arrive to the simple conclusion that in spite crop 2018 will be for sure below 36 millions tons, considering that today consumption is probably at about 37 millions tons, we are only reducing the above forecast carryover by one million tons !

This means we would need more small productions in the following crops if producers want to drive the market back to a more balanced situation.

However from a market point of view we all know that China is normally the driving factor for the price drop and consequently the very small Chinese crop will probably help to keep a price to a more reasonable level.

The global financial stress is rapidly increasing and more industries are losing money all over the world and the Chinese development is confirming that we are probably arriving to a limit no longer sustainable.

Finally the industries are facing a crisis which is not connected to a sudden production increase (often happening in the past) but to a change of the model of the economic reference, a systemic crisis which would require a different long term approach and strategy.

Unless global consumption is suddenly increasing again, will industries be able to challenge the new model ?

Have a nice crop !

Armando Gandolfi